Imagine you're climbing to the top of your career as a self-employed person, skillfully handling your business. But suddenly, you come across an unexpected challenge, a serious illness or injury that stops you from working. Or even more worrying, think about what would happen to your family if you were no longer there. How would your mortgage- often the biggest monthly bill your family has to handle?

That's where mortgage loan protection insurance steps in, ensuring your family's home remains secure. Designed to take care of your mortgage in these critical times, MPI acts as a protective barrier, allowing you and your family to keep your home and maintain your lifestyle without the stress of mortgage payments during tough times.

What is Mortgage Protection Insurance?

Mortgage protection insurance is a type of life insurance policy specifically tailored to cover your mortgage repayments in the event of life-altering situations such as death, disability, or a severe illness.

Have you ever wondered what would happen to your home if you suddenly couldn't work or weren't there anymore? This insurance ensures that your most significant financial commitment, your home mortgage, is taken care of, keeping your family's living situation secure and stable.

But what does this mean for you and your family? It means that in times of unexpected hardship, you won't have to worry about how mortgage payments will be met or how much life insurance do I need to maintain your family's stability.

This peace of mind is invaluable, isn't it? Mortgage protection insurance provides a safety net, ensuring that your family can continue living in their home without the burden of financial instability during challenging times. By safeguarding your home's financing through a reliable insurance broker, you're also protecting the heart of your family's daily life and long-term security.

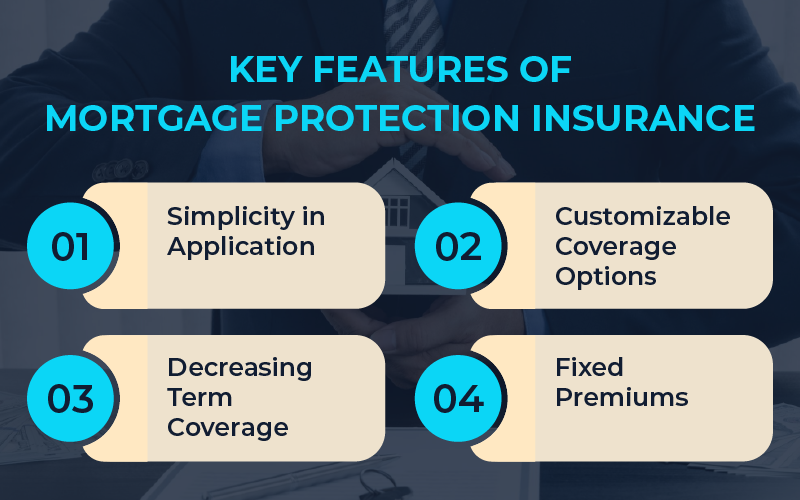

Key Features of Mortgage Protection Insurance

Here are some of the features that define mortgage protection insurance-

Simplicity in Application - Unlike traditional life insurance, applying for MPI is usually straightforward, often requiring no medical exam, making it an attractive option for the busy self-employed individual.

Customizable Coverage Options - You can select coverage amounts based on your mortgage balance and your other financial needs, allowing you to customize the policy to fit your specific scenario.

Decreasing Term Coverage - The amount of coverage typically decreases over time, paralleling the decline of your mortgage balance. This keeps the policy affordable while still matching your needs.

Fixed Premiums - Many mortgage loan protection insurance policies offer fixed premiums for the duration of the policy, providing predictable costs without unexpected increases.

What Does It Cover?

Mortgage protection insurance steps in to cover critical aspects of your mortgage when you face hardship.

Death - In the event of your death, MPI pays off your entire mortgage, leaving your family free from financial burdens and allowing them to keep their home. For instance, imagine a self-employed graphic designer with an MPI policy. After an unexpected illness, the designer passes away, leaving behind a family. The mortgage insurance in case of death kicks in, paying off the remaining amount on their home mortgage, ensuring the family stays in their home without the burden of monthly mortgage payments.

Disability - If you're temporarily unable to work due to illness or injury, MPI can cover your mortgage payments for a specified period, often ranging from 12 to 24 months. For example, if your leg breaks and you can't work for several months. Then your MPI covers the mortgage payments during the recovery period, easing the stress of meeting that significant expense while focusing on healing.

Critical Illness - Some policies extend coverage to include critical illnesses like cancer, heart attack, or stroke, providing lump-sum payments to help cover the mortgage. For example, think about a self-employed consultant diagnosed with a critical illness. The consultant's MPI policy provides a lump-sum payment that covers the mortgage, allowing the use of other savings to focus on treatment and recovery without the added stress of house payments.

What Does It Not Cover?

While MPI is comprehensive, it doesn't cover everything. Some of the common exclusions include-

Pre-existing Health Conditions - Many mortgage insurance in case of death policies will not cover disabilities or deaths due to health issues known before the policy was purchased.

Voluntary Job Loss or Unemployment - Losing your job or quitting voluntarily doesn't qualify for coverage under most property mortgage insurance (MPI) policies.

Short-Term Illness or Minor Injuries - Shorter illnesses or minor injuries that don’t significantly impact your ability to work might not be covered in this insurance.

Certain Types of Deaths - Some policies exclude coverage for deaths due to high-risk activities or certain natural causes.

Important Things You Need to Know About MPI vs. PMI vs. MIP

These three types of life insurance serve different purposes, so comparing all of them isn't necessary to select the optimal mortgage protection option. The following table will help you quickly differentiate among them, ensuring that you don’t get confused.

Here are the key differences you really need to know about these three types of life insurance:

| Feature | MPI (Mortgage Protection Insurance) | PMI (Private Mortgage Insurance) | MIP (Mortgage Insurance Premium) |

| Purpose | To protect the borrower's ability to repay the mortgage in case of death, disability, or certain illnesses. | To protect the lender from the risk of default and foreclosure if the borrower stops making payments. | Required for FHA loans to protect lenders from the risk of default and foreclosure. |

| Paid By | Borrower | Borrower | Borrower |

| When It’s Required | Optional; the borrower chooses to take it out to protect their family or estate. | Usually necessary in cases where the down payment is less than 20% of the purchase price. | Required for all FHA loans, regardless of the amount of the down payment. |

| Premiums | Fixed or variable; paid monthly, quarterly, or annually. | Fixed; paid monthly as part of the mortgage payment. | Fixed; paid monthly as part of the mortgage payment and at closing. |

| Cancellation | Can be cancelled at any time by the borrower as it is not required by lenders. | Can be cancelled once the mortgage balance falls below 80% of the home’s value under certain conditions. | MIP cannot be cancelled on loans with an initial down payment less than 10%; otherwise, it can be cancelled after 11 years. |

| Benefits | Provides peace of mind and financial stability for the borrower’s family by paying off the mortgage in case of the borrower's death or disability. | Allows borrowers to buy a home with a smaller initial payment. | Enables borrowers to qualify for an FHA loan with a down payment as low as 3.5% of the home's price. |

| Duration | Matches the term of the mortgage (e.g., 30 years). | Remains in place until the loan-to-value ratio reaches 78-80% or based on the borrower’s request at 80%. | For the life of the loan or until the loan-to-value ratio reaches a certain point, depending on the specifics of the FHA loan. |

Conclusion

Have you ever wondered how your family would manage without your income during a crisis? Mortgage protection insurance provides the answer, ensuring that you won't have to. By understanding the ins and outs of mortgage protection insurance, from what it covers to what it doesn’t, you can make an informed decision that enhances your financial safety net.

So, why wait? Take the step today to explore this essential coverage with Sater Insurance and continue building your life on a foundation of security and stability. Your family will thank you for choosing a partner like Sater Insurance, dedicated to protecting your dream and your home.