When most people think of life insurance, they often focus on the death benefit—the payout that beneficiaries receive after the policyholder passes away. But did you know that life insurance can also offer significant benefits while you’re still alive? These are known as living benefits.

Have you ever wondered how these benefits can help you?

Let’s explore what living benefits are, how they work, and the specific advantages they offer through different types of life insurance policies. You’ll be surprised at how much value life insurance can provide during your lifetime!

What is Life Insurance?

An agreement between you and the insurance provider is a life insurance policy. You pay regular premiums, and in return, the insurer promises to pay a sum of money to your beneficiaries upon your death. But life insurance isn’t just about the death benefit—it also offers valuable living benefits.

For example, you’re a parent with young children.

You purchase a whole life insurance policy to ensure your family is financially secure if something happens to you. Years pass, and you’re diagnosed with a serious illness.

Thankfully, your policy includes an accelerated death benefit rider, allowing you to access a portion of your death benefit to cover medical expenses, reducing your financial stress. This is a real-life example of how life insurance can provide critical support when you need it most.

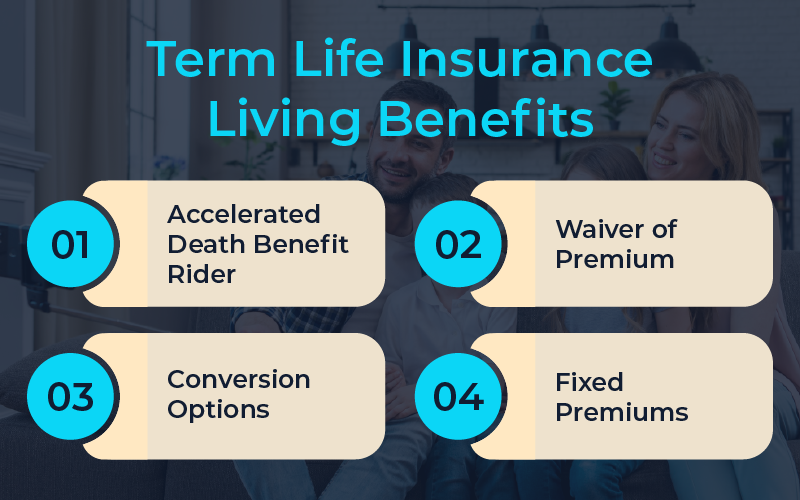

Term Life Insurance Living Benefits

Term coverage life insurance is a popular choice for those seeking affordable coverage for a specific period, such as 10, 20, or 30 years. While it doesn’t typically offer the same range of living benefits as permanent life insurance, there are still important advantages to consider.

- Accelerated Death Benefit Rider-

This allows policyholders to access a portion of the death benefit if diagnosed with a terminal illness. For example, a policyholder diagnosed with a terminal illness can use this benefit to cover expensive medical treatments, reducing financial stress on their family.

- Waiver of Premium-

If the policyholder becomes disabled and unable to work, this rider waives the premium payments, keeping the policy active without additional cost. For instance, a policyholder who becomes disabled after an accident would no longer have to worry about paying premiums, ensuring their policy remains in force.

- Conversion Options-

Some term life policies offer the option to convert to a permanent life insurance policy without a medical exam, allowing policyholders to extend their coverage and access permanent life-living benefits. For example, a policyholder nearing the end of a 20-year term policy can convert it to a whole-life policy, securing lifelong coverage without the need for a medical examination.

- Return of Premium-

Some term life insurance policies offer a return of premium option, which gives back all the premiums if the policyholder outlives the term. For example, a policyholder who pays term life insurance premiums for 20 years and remains in good health at the end of the term receives all premiums back, essentially providing no-cost coverage.

Permanent Life Insurance Living Benefits

Permanent life insurance, such as whole life insurance, universal life insurance, and variable life insurance, offers lifelong coverage and a variety of living benefits. Here are some key benefits-

- Cash Value Accumulation-

One of the most significant advantages of whole life insurance and other permanent policies is the cash value component, which grows over time and can be borrowed against or withdrawn. For example, if a policyholder needs funds for a major home renovation, they can borrow against the cash value of their policy, providing a convenient source of low-interest funds.

- Policy Loans-

Policyholders can take out loans against the cash value of their life insurance with cash value. These loans usually don’t involve credit checks and have accessible interest rates. For instance, a policyholder facing unexpected medical expenses can quickly obtain a loan from their policy’s cash value, avoiding high-interest credit card debt.

- Benefits for Chronic Illness-

Some policies provide benefits if the policyholder becomes chronically ill and unable to perform daily activities, offering financial support for long-term care. For example,When a policyholder detects a diagnosis of a chronic condition, like Alzheimer’s, they can use the money from their policy to pay for in-home care services, guaranteeing they get the assistance they need without using up all of their savings.

- Universal Life Insurance Flexibility-

Universal life insurance offers flexible premium payments and death benefits, allowing policyholders to adjust their coverage as their financial needs change. For instance, if a policyholder experiences a reduction in income, they can reduce their premium payments temporarily while still maintaining their coverage, or increase their death benefit as their financial responsibilities grow.

- Tax-Deferred Growth-

The cash value in a permanent life insurance policy grows on a tax-deferred basis, meaning policyholders do not pay taxes on the gains until they withdraw the money. For example, a policyholder who allows their cash value to grow over many years can accumulate a significant amount of money, which can be used for retirement income or other financial goals, without having to pay taxes on the growth until they withdraw the funds.

Conclusion

Exploring the living life insurance benefits shows how they support you beyond just a death benefit. Have you considered how these benefits could enhance your financial security? From covering medical expenses to providing flexible premium payments, living benefits offer significant advantages.

For personalized advice and to find the best policy for your needs, contact Sater Insurance. Discover how life insurance can be a valuable asset for you and your loved ones today.

Why wait? Start securing your future with Sater Insurance now!

FAQ’s

- What are examples of living benefits?

Living benefits in life insurance include accessing part of your death benefit if diagnosed with a terminal illness, using cash value for loans or withdrawals, and receiving support for chronic illness care. These benefits can help cover medical expenses, fund significant purchases, and provide financial flexibility while you’re still alive.

2. What type of life insurance has living benefits?

Both term and permanent life insurance can have living benefits. Term life insurance offers benefits like early payouts for serious illness. Permanent life insurance, such as whole or universal life, provides benefits like cash savings you can use or borrow, and support if you get seriously ill. These benefits help you financially while you’re still alive.